The future of the Eurozone

In the few days prior to 8 May 2010, European country leaders noticed a rapid loss of market confidence in government bonds. This loss of confidence not only affected bonds issued by the Greek government but also government bonds of several other member countries in the eurozone. The default insurance premium on government bonds picked up rapidly for several countries, indicating that the market participants had revised their expectations about these governments’ ability and/or willingness to honour their outstanding debt.

by Kai A. Konrad and Holger Zschäpitz

Original Article in: CESifo Forum 2/2011

Country leaders reacted. Within two days they constructed what is known as the 750 billion euro rescue device. It consisted of the EFSF, the EFSM and additional guarantees provided through the International Monetary Fund. In hindsight, some policy makers admit that the initial idea was that a European promise of support of this size would be sufficient to re-establish confidence among market participants. The hope may have been that market participants return to their prior expectations about government bonds of members of the eurozone: holding these bonds are perfectly safe assets, with bonds of different countries being almost perfect substitutes for each other.

Now, one year later, it is evident: their policy went completely wrong. In addition to the 110 billion euro rescue package for Greece, the governments of Portugal and Ireland had to be rescued. They received considerable financial aid from the rescue device, and other countries like Spain or Italy are candidates that may follow. And the insurance premiums for many of the relevant countries – including the ones rescued – are higher in May 2011 than they were in May 2010.

Officially, Greece was supposed to return to the private capital market after a period of no more than three years. But rather than an improvement in credit worthiness, during the last 12 months we have seen a process of deterioration. Rather than preparing for a return to the private capital markets, Greece entered into debt renegotiations about prolonging the help and easing the debt burden further. There is seemingly almost a consensus that Greece cannot reach a financially healthy situation without either a partial devaluation of its debt in the process of a default followed by a debt restructuring, or massive foreign transfers.

It is difficult to admit a mistake, in particular a mistake of this size. Not surprisingly the policy reaction to the failure is not a change of direction, but rather: ‘what we did was right, but it was not enough’. Projecting this behaviour into the future, a likely direction of European policy is a speedy integration of fiscal policy inside the eurozone. First steps in this direction took place. We see the modifications of the Stability and Growth Pact that include a view on macroeconomic imbalances in member countries, the intensified reporting and benchmarking in the context of the ‘European Semester’ and of the ‘Euro Plus’ agreements as part of this process. These instruments clearly strengthen the position of the European Commission inside the European Union, expand on existing tasks and allocate new tasks to the bureaucracy of the European Commission.

We are doubtful whether these steps will cure the European government debt crisis. It is very likely that, given these steps, the problems will persist and may even grow further. At some point in the near future policy makers in the eurozone will have to take further steps.

As we emphasized (Konrad and Zschäpitz 2010) already at the brink of introduction of the rescue device in May 2010, there are several, very different policy options. One option is a complete reversal of the steps towards socialized fiscal responsibility that have been taken in the last months and a return to a status of national fiscal responsibility. This step implies that some member countries that suffer from a severe fiscal imbalance are likely to face the prospect of a debt restructuring, whereas others may need to take very painful steps to return to sound public finances. As pointed out by Reinhart and Sbrancia (2011), ‘financial repression’ may be one policy options taken by the latter.1 Politics wasted very valuable time which they had bought for themselves by the rescue device in May 2010 so far. Policy makers in Europe could still use the time window that exists. Along this way, they need to make the banking system in Europe and the financial markets more generally sufficiently resilient and robust to sustain such a period of crisis. We emphasized this as a necessity from the beginning of the crisis (Konrad and Zschäpitz 2010), and the Council of Scientific Advisors to the Federal Ministry of Finance in Germany (2010) followed a very similar line of reasoning.

This policy would, among other things, require a strong separation of the banking system and the business of financing government debt. The fact that private banks own considerable shares in European government bonds and risk a major share of their equity in this market makes a restructuring more difficult than otherwise. We understand why, under current conditions, banks have an interest in investing their assets in government bonds. Under current regulation, they need less equity to finance such investments than if they hand out loans to medium-size enterprises. This clearly is like a subsidy by which the governments distort banking decisions, making banks more inclined to finance government debt than engage in their core business. And from the perspective of political economy, this type of subsidy is not difficult to understand. But from the perspective of economy wide efficiency, we do not see a convincing reason why banks should use (or should even be stimulated to use) their own funds to invest it in government bonds. They should leave this business to insurance companies, pension funds and small private investors and should turn to their core business as it is outlined in the textbooks about banking business.2 As discussed, the political process since 10 May 2010 did not march in this direction, but drifted into the opposite direction. Many key players inside the eurozone seemingly wanted to rule out state bankruptcy inside the eurozone. Early on, the German Chancellor considered intergovernmental transfers or financial aid as the ‘ultima ratio’, where economists would consider a process of default and debt restructuring as the more adequate ultima ratio. We expect that the political process will drift further into this other direction, essentially further socializing financial responsibility, and generating a common pool as regards European government debt.

European leaders may first try to implement fiscal sustainability via strengthening supervision and by a modified enforcement mechanism with sanctions for excessive government deficits, together with strict conditionality in case a country has to rely on fiscal aid from the newly installed European Stability Mechanism. We are convinced that this will not work. And once these attempts have failed, this could, directly or indirectly, lead to a dramatic expansion of the system of financial transfers between the member countries inside the eurozone or the EU as a whole: a system in which a constant flow of funds from countries with sound public finances prevents some other countries from bankruptcy.

Such a transfer system exists in a rudimentary version in the context of the common agricultural policy and in the context of cohesion funds as part of EU policy. This argument is frequently used to suggest that a transfer union is not a dramatic change, compared to the status quo. But this argument drastically downplays such a change. To make this very transparent, it may be useful to get a feeling for the magnitude of the fiscal transfers we would observe if we simply scaled a system such as the system of intergovernmental transfers in Germany between the regions to the European level. Nobody, as far as we know, proposes such a system in the current state of affairs. And this thought experiment is, of course, not meant as a policy proposal here either. It is meant as an illustration of the excessively large sums that are at stake if the EU moved towards a transfers union of any kind.

The German federal transfer system aims at a strong reduction in the interregional differences in governmental revenue per capita. Loosely speaking, and subject to some more specific rules, this system takes from those states who obtain tax revenues per capita that are above average in Germany, and reduces the difference of states with lower-than-average tax revenues. The degree of equalization of per-capita tax revenue between the different states in Germany is above 90 percent.

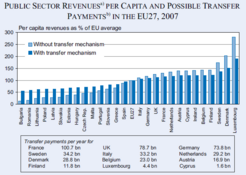

Figure 1 shows the public sector revenues (sum of taxes and social security contributions) on a percapita basis for the 27 member states of the European Union as a percentage of the EU average for the year 2007, which is the last year that is not substantially affected by the financial and economic crisis. This figure shows that the discrepancies between the member countries are dramatic. For instance, the public sector revenue in Bulgaria is in the range of only about 12.6 percent of the EU average. Consider a transfer mechanism that eventually redistributes revenues between member countries that cover only half of the difference between this actual level and the EU. The revenues of Poland, for instance, are 27.8 percent of the EU average. If fifty percent of the deviation from this average is corrected for, Poland would receive half of 72.2 percentage points. This increases fiscal revenue to 63.9 percent of the EU average. This transfer would have to be financed by the countries that have fiscal revenues above the EU average. For the year 2007 the fiscal revenue of Germany exceeds that of the EU average by around 17.6 percent. A transfer mechanism that simply equalizes 50 percent of the difference from average, based on 2007 figures, sums up to 445 billion euros per year. For Germany, for instance, this would be a contribution of almost 74 billion euros per year, on the basis of the 2007 figures.

These numbers were calculated for a transfer mechanism that builds on social security inclusive figures. One may claim that this is a misleading comparison, and that one should focus on tax revenues only. This would reduce the numbers, as on average tax revenues are only two thirds of the social security inclusive numbers we used for these rough calculations. However, this would still be excessively large numbers.

Evidently, these numbers are not related to any of the policy proposals that is currently negotiated. Nevertheless, these numbers are interesting, for several reasons. These rough calculations show: a transfer mechanism that achieves little more than half the amount of equalization in governmental revenues would have transfers that are magnitudes larger than the total current EU budget. Currently all EU member countries receive back a large share of their contributions to the EU budget via the different EU programmes. The current net transfers inside the EU are much smaller than the total EU budget. Accordingly, the net transfers would be orders of magnitude larger than the current net transfers between EU member countries.

These considerations illustrate: the hint to the fact that the EU already is a transfer union really down plays the dimension of the problem. We may also recall that already the existing net transfers that are tiny in comparison to the numbers in Figure 1 are the cause of a permanent struggle inside Europe. It is hard to believe that Europe could survive the political antagonisms that would be created by transfers of this magnitude.

Second, implementation of a transfer system of any kind would not be a trivial matter. Any transfer mechanism that takes from countries with high tax revenue and gives to those with little tax revenue generates considerable incentives inside the countries for reductions in their own tax revenues. Leaving the income in the pockets of their citizens and receiving tax revenue via a European transfer mechanism is seemingly more attractive from a country’s national point of view than charging own citizens high taxes and using the tax revenue as transfers to other countries. And given that tax laws are non-uniform across the European Union, the member countries would have incentives to lower tax rates, or to abolish a major share of their taxes: low taxes would benefit their own population directly, and a large share of the tax revenue sacrificed would be compensated by higher transfers from other member countries. Accordingly, any substantial inter-country transfer system of tax revenues could not work without a considerable increase in tax law harmonization. It would require a further large step toward ‘European integration’. Whether this is really a desirable and politically viable option for a future Europe is a different matter.

A transfer union of the type described here is clearly not a desirable perspective. And the massive volume of transfers is also unlikely to be economically or politically viable. Although such a transfer union could be the logical endpoint of the path which European policy makers are currently pursuing, we consider a transfer union of this type as unlikely. A more likely outcome is a breakdown of the eurozone prior reaching this endpoint. One possible reason for this breakdown is a raise in political tensions among member countries. A second, more likely reason is the bond market’s possible loss of confidence in the sustainability of the whole eurozone.